Investment Looks Like Damage From Outside

By Jack Butcher

Free cash flow drops. The headlines write themselves. Analysts flag the decline. Investors get nervous. Everyone agrees something is wrong.

Sometimes nothing is wrong. Sometimes the company is doing exactly what it should.

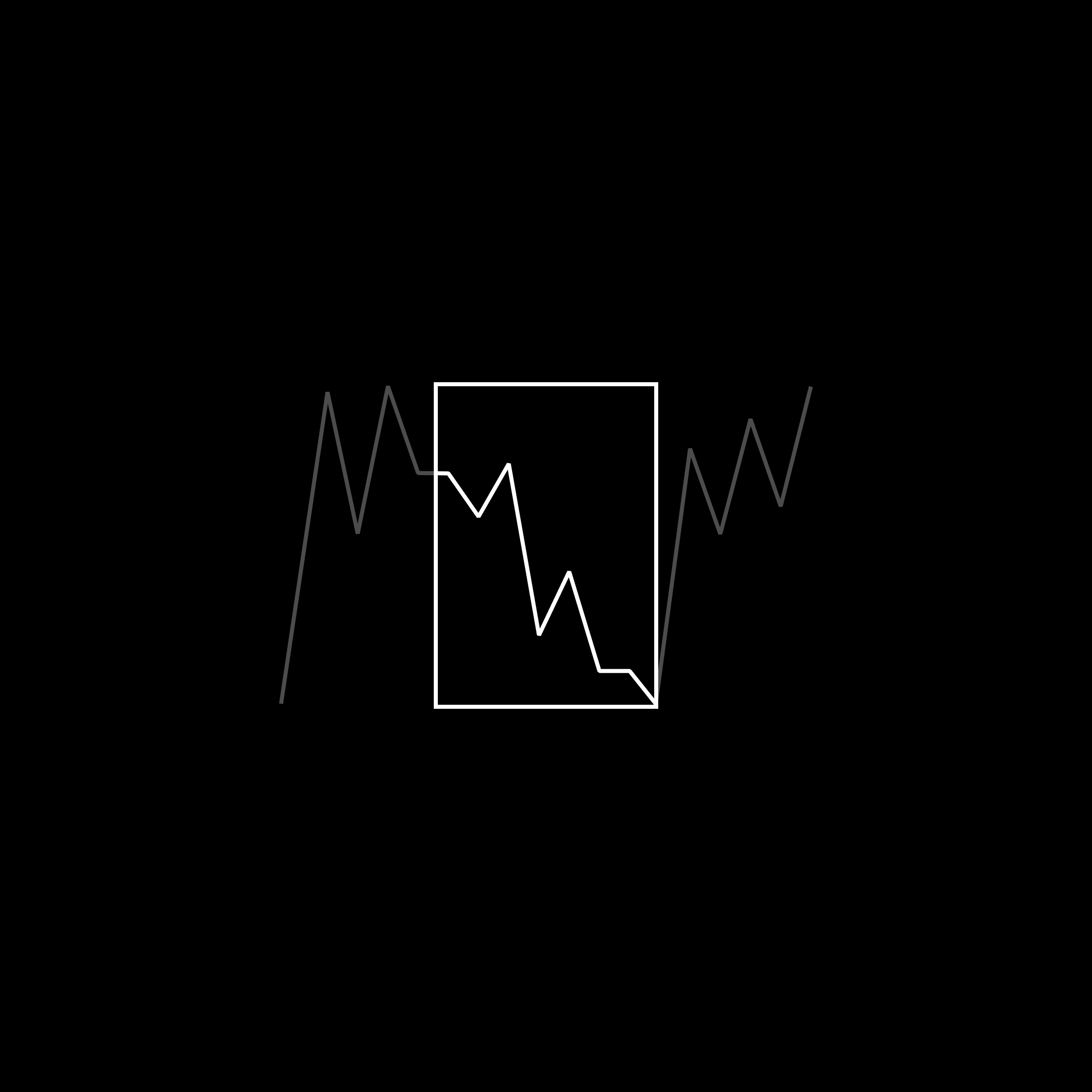

Free cash flow is operating cash flow minus capital expenditure. That second number matters more than most people give it credit for. When a company decides to build — seriously build, at scale, for years — capital expenditure spikes. Operating cash flow stays roughly steady or grows, but the gap between the two compresses. Free cash flow falls. From the outside, it looks like deterioration. From the inside, it is the strategy executing on schedule.

The hyperscalers are in this cycle right now. Data centers, chips, infrastructure, compute capacity that doesn't exist yet and needs to exist before the demand fully arrives. You don't build that cheaply. You don't build that quickly. And you don't build that without the numbers looking ugly on a quarterly basis to anyone who isn't paying attention to what the numbers actually represent.

The error is treating free cash flow as a single signal when it is the output of two very different inputs. Operating cash flow collapsing is a warning. Capital expenditure surging is, in many cases, a bet. Confusing one for the other is how you misread a company at exactly the moment it matters most.

A business that is genuinely deteriorating shows declining operating cash flow. Revenue softens, margins compress, the core engine loses power. That's damage. A business in heavy investment mode shows rising capex against stable or growing operating cash flow. The engine is fine. They're just building more engines.

The distinction is not subtle, but it gets missed constantly because the outcome — lower free cash flow — looks identical in the short term. Damage and investment produce the same number. They do not produce the same future.

This is why time horizon is everything in how you read a balance sheet. A short enough window makes any serious investment look like failure. Zoom out and the same numbers tell a completely different story — a company converting operating cash flow into durable infrastructure, trading liquidity today for capacity tomorrow.

The companies spending the most aggressively on capex right now are doing so because they believe the demand coming will dwarf the infrastructure available to serve it. They are not spending because they have excess capital and nowhere better to put it. They are spending because the cost of underbuilding outweighs the cost of overbuilding. That calculus might be wrong. But it is a considered bet, not a sign of distress.

Reading a falling FCF number and concluding the business is in trouble without asking why the capex is elevated is like reading a construction budget and concluding the company is losing money. The spend is the point. The temporary compression of free cash flow is the price of the position.

The investors who get this right aren't smarter. They're just asking the second question. The first question is: what is the free cash flow? The second question is: what is consuming it, and why?

One question gives you a number. Two questions give you a picture.

Go deeper.

Install the full system — lessons, tools, workflows, and everything we build. $99/year.

Stay in the loop.

New ideas, tools, and work. No spam.

Visuals

View All